What if every pound you earned had a specific destination — before you spent a single penny of it? That’s the premise behind zero-based budgeting (ZBB), and it’s the reason YNAB has a near-cult following, and why millions of people use it to eliminate debt and build genuine wealth.

This guide explains what zero-based budgeting is, how it differs from traditional budgeting, how to set it up yourself, and which tools make it effortless in 2026.

| What You’ll Learn

By the end of this guide you’ll understand the zero-based method completely, know whether it’s right for your life, and have a step-by-step plan to implement it today — for free. |

What Is Zero-Based Budgeting?

Zero-based budgeting is a method where your income minus your planned expenditure equals zero. Every single pound of income is deliberately allocated to a category — whether that’s rent, groceries, debt repayment, or savings.

The key insight: zero doesn’t mean broke. It means every pound has a job. When you assign £200 to your emergency fund, that £200 isn’t ‘missing’ — it’s working towards a goal.

The Formula

| Monthly Income − All Allocated Amounts = $0 (or £0 / €0)

Every dollar/pound/euro you earn is given a purpose. Nothing is left ‘floating’. |

Zero-Based Budgeting vs Traditional Budgeting

Related: → Zero-Based Budgeting vs Traditional Budgeting: Which Actually Works in 2026?

| Traditional Budgeting | Zero-Based Budgeting | |

| Starting point | Last month’s budget | Start from zero every month |

| Leftover money | Rolls over untouched | Reassigned to a goal or savings |

| Level of control | Low — broad category limits | High — every $1 has a specific job |

| Time required | Low — set and forget | Medium — requires active review |

| Best for | Stable expenses, low debt | Debt payoff, aggressive saving |

| Mental shift | Reactive (track what happened) | Proactive (plan what will happen) |

Who Should Use Zero-Based Budgeting?

Zero-based budgeting is particularly powerful for:

- People living paycheck-to-paycheck who can’t figure out where the money goes

- Anyone trying to pay off significant debt aggressively

- Households where one partner earns variable income

- People who have tried budgeting before but keep drifting

- Anyone saving for a major goal (house deposit, wedding, early retirement)

It may not be the right fit if:

- Your income varies wildly month-to-month and you find rigid planning stressful

- Your expenses are already well-managed and you want a simpler overview approach

- You’re primarily focused on investment and net worth tracking rather than day-to-day spend control

| Good News

You don’t have to choose between zero-based control and modern convenience. EMOH Pay supports flexible budgeting that blends zero-based allocation with automated expense tracking — giving you full control without the manual work. |

How to Set Up Zero-Based Budgeting: Step-by-Step

Step 1: Calculate Your Total Monthly Income

Include all income sources: salary, freelance earnings, rental income, benefits, child support. Use net (after tax) figures. For irregular income, use the lowest month from the past 6 as your baseline.

Step 2: List Every Single Expense Category

Start with the non-negotiables (fixed expenses), then move to variables:

- Fixed: Rent/mortgage, insurance, loan repayments, phone, internet

- Variable necessities: Groceries, transport, utilities, medical

- Discretionary: Dining out, entertainment, clothing, personal care

- Savings & investments: Emergency fund, pension, ISA/RRSP/401k, savings goals

- Debt repayment: Any amounts above minimum payments

Step 3: Assign Every Pound a Category

Start allocating your income across your categories, non-negotiables first. Work down through necessities, then discretionary spending. What remains must go to savings or debt.

The golden rule: income minus all allocations must equal zero. If you have money left over, assign it — to savings, a holiday fund, or accelerated debt repayment. If you’re over budget, cut somewhere.

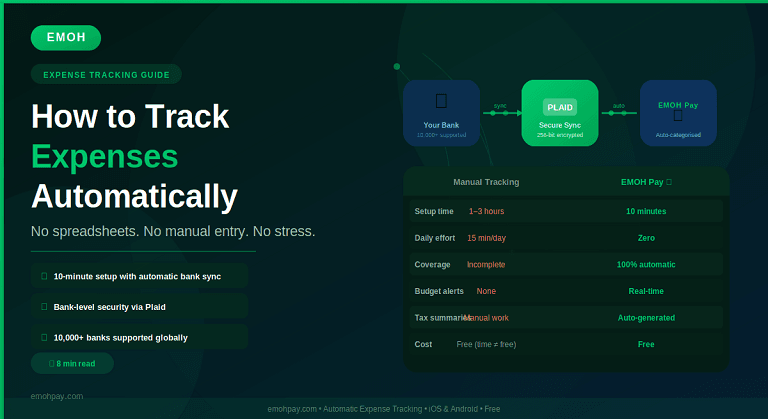

Step 4: Track Every Transaction

Zero-based budgeting only works if you track spending in real time. This is where manual ZBB systems fail — it’s simply too tedious. This is why pairing ZBB with EMOH Pay’s automatic expense tracking makes the method sustainable.

Set up automatic tracking: → How to Track Expenses Automatically

Step 5: Adjust Allocations Mid-Month When Needed

Life doesn’t follow a plan perfectly. When you overspend in one category, you must reduce another — this is the discipline that makes ZBB work. With EMOH Pay, you can adjust category budgets in real time and see the knock-on effect instantly.

Step 6: Review and Reset at Month End

At the end of each month, check every category. Assess what worked, what didn’t, and adjust next month’s allocations accordingly. Most ZBB users find they need 3 months to calibrate their budgets accurately.

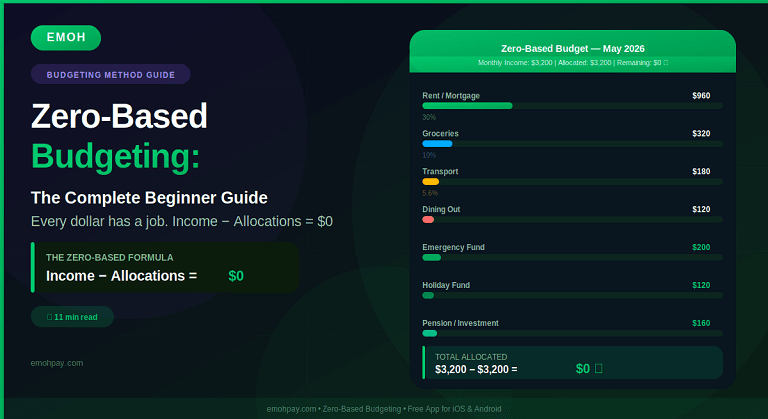

Zero-Based Budgeting Example (Monthly, £3,000 Take-Home)

| Category | Budget | % of Income | Notes |

| Rent/Mortgage | $900 | 30% | Non-negotiable — first allocation |

| Groceries | $300 | 10% | Use EMOH Pay tags per family member |

| Transport | $200 | 6.7% | Car, fuel, public transport combined |

| Utilities | $150 | 5% | Gas, electricity, water |

| Phone & Internet | $80 | 2.7% | Fixed cost — review annually |

| Insurance | $120 | 4% | Car, home, life |

| Dining Out | $150 | 5% | Budget for enjoyment, not guilt |

| Entertainment | $100 | 3.3% | Streaming, events, hobbies |

| Clothing | $80 | 2.7% | Adjust seasonally |

| Personal Care | $50 | 1.7% | Haircuts, toiletries |

| Medical Buffer | $50 | 1.7% | Pharmacy, dentist, prescriptions |

| Gift & Celebrations | $50 | 1.7% | Spread Christmas/birthday spend evenly |

| Emergency Fund | $200 | 6.7% | Until 3 months’ expenses saved |

| Pension/Investments | $300 | 10% | Pay yourself first |

| Holiday Fund | $100 | 3.3% | Sinking fund — goal set in EMOH Pay |

| Debt Repayment | $170 | 5.7% | Above minimum payments |

| ━━ TOTAL | $3,000 | 100% | Income − Allocations = $0 |

Common ZBB Mistakes (And How to Avoid Them)

- Forgetting irregular expenses: Annual subscriptions, car tax, birthday gifts. Solve this with sinking funds in EMOH Pay — set aside a small monthly amount for each.

- Being too rigid at the start: Your first ZBB month will be wrong. That’s normal. Budget loosely in Month 1, tighten in Month 2 and 3 as you learn your real patterns.

- Not tracking every transaction: ZBB without tracking is guesswork. Connect EMOH Pay for automatic tracking so no expense slips through.

- Forgetting savings as an ‘expense’: Savings aren’t what’s left after spending — they’re a line item just like rent. Allocate them first.

Frequently Asked Questions

Q: Does zero-based budgeting mean spending everything?

No. In ZBB, every pound has a job — which means your savings, pension, and investment contributions are ‘expenses’ in your budget too. When income minus all allocations equals zero, it means nothing is floating around unassigned, not that your account is empty.

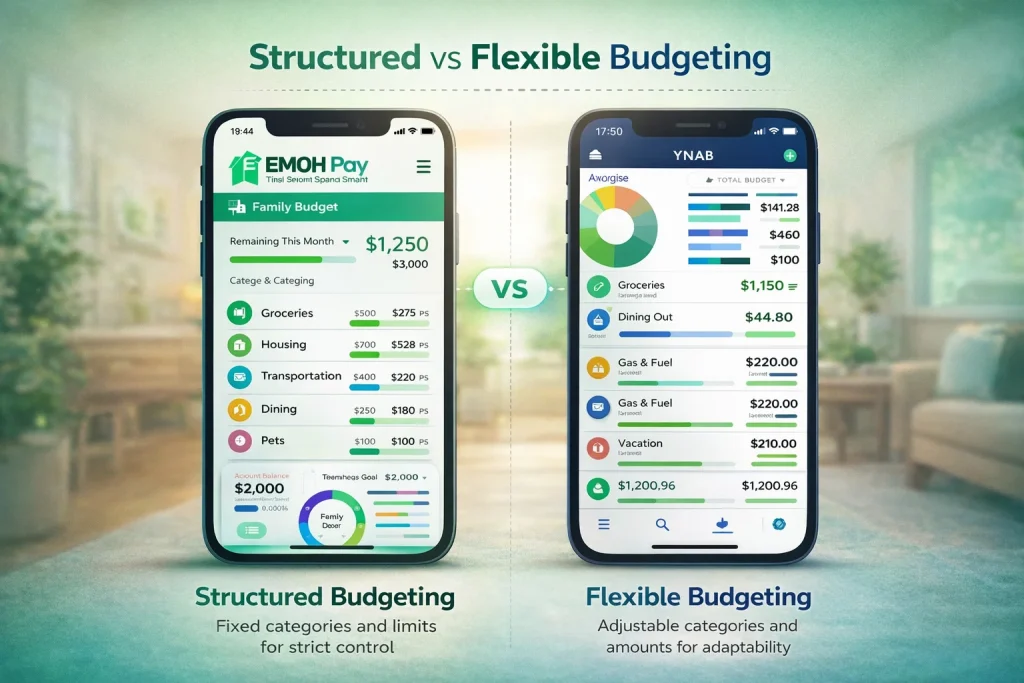

Q: How is zero-based budgeting different from the envelope method?

They are similar in philosophy but different in mechanics. ZBB allocates income to categories mathematically. The envelope method traditionally uses physical cash in labelled envelopes. Digital apps like EMOH Pay let you implement both concepts — set category budgets (ZBB) with visual limits (envelope concept) without using physical cash.

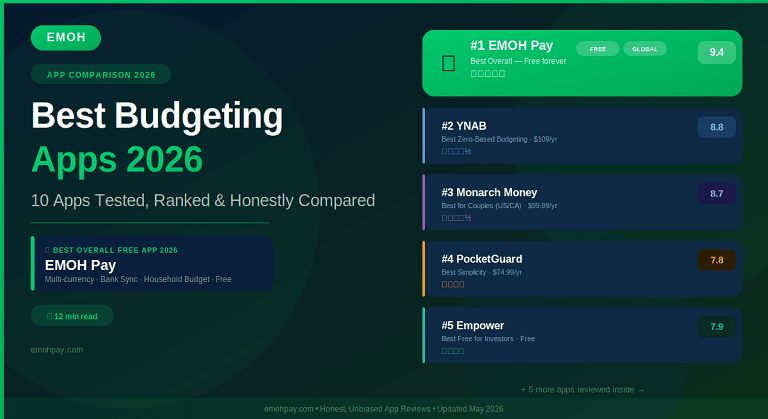

Q: What app is best for zero-based budgeting?

YNAB is the most dedicated ZBB app but costs $109/year. EMOH Pay offers flexible zero-based budgeting with automatic bank sync and household features completely free — making it the best free option for ZBB in 2026.

Q: How long does zero-based budgeting take to set up?

Your first budget will take 30–60 minutes to set up properly. Subsequent months take 15–20 minutes to review and reset. With EMOH Pay, automatic transaction import cuts the daily maintenance to near zero.

| Ready to Take Control of Your Finances?

Download EMOH Pay Free — Available on iOS & Android App Store: apps.apple.com/pk/app/emoh/id6743326641 Google Play: play.google.com/store/apps/details?id=com.buildmeapp.emoh |

Continue Your Budgeting Education

→ The Ultimate Guide to Budgeting in 2026

→ Zero-Based vs Traditional Budgeting: Which Actually Works?

→ Best Budgeting Apps 2026: Tested & Ranked