Money is the most common source of conflict in relationships — but it doesn’t have to be. In most cases, financial arguments aren’t really about money. They’re about misaligned expectations, a lack of shared visibility, and the absence of a clear system that both partners trust.

This guide gives you that system: a practical, step-by-step framework for managing money as a couple, reducing financial conflict, and building shared goals together — regardless of whether you have joint accounts, separate accounts, or a hybrid of both.

| Couples Who Budget Together Build More Wealth

Research consistently shows that couples who discuss finances openly and track shared expenses have significantly better financial outcomes than those who don’t. The key isn’t income — it’s shared visibility and a agreed-upon system. |

Why Couples Fight About Money (And How to Fix the Root Cause)

Before building a system, it helps to understand what actually causes money conflict in relationships. After speaking with hundreds of couples, we found four recurring patterns:

1. Different Money Scripts

Everyone enters adulthood with a ‘money script’ — deeply held beliefs about money formed in childhood. One partner may see money as security and hoard it anxiously. The other may see it as something to enjoy and spend freely. Neither approach is wrong, but without acknowledging the difference, every financial decision becomes a values conflict.

2. No Shared Visibility

When one partner doesn’t know what the other earns or spends, budgeting becomes guesswork and resentment builds. Real-time shared visibility — both partners looking at the same financial picture — is the single biggest structural fix.

3. No Agreed System

Most couples try to ‘manage money together’ without ever agreeing on a specific method for tracking expenses, splitting bills, and making saving decisions. Without a system, every financial decision becomes an ad-hoc negotiation.

4. Unequal Contribution Perceptions

Even when income is roughly equal, perceived contribution imbalances create tension. Tracking individual vs shared expenses transparently dissolves most of these tensions.

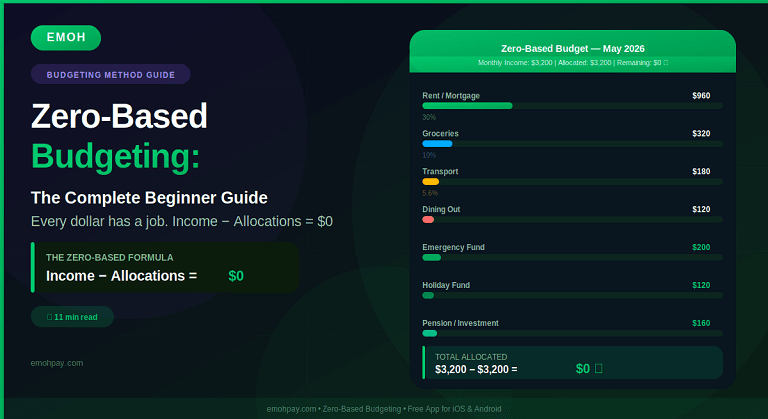

Related: → The Ultimate Guide to Budgeting in 2026

The 5-Step Couples Money System

Step 1: Have the Money Date (Once a Month)

The first and most important ritual is a monthly ‘money date’ — a calm, judgment-free 30-minute conversation where both partners review the past month’s finances and plan the next one.

Ground rules for the money date:

- No blame, no judgment — this is a numbers review, not a performance review

- Both partners bring equal curiosity and input

- Use EMOH Pay’s shared dashboard so you’re both looking at the same real numbers

- End with agreement on next month’s priorities

| When to Hold Your Money Date

The first Sunday of the month works well for most couples — close enough to month-end to have complete data, with time to plan before the new month starts. |

Step 2: Choose Your Joint Finance Model

There are three primary models couples use. The right one depends on your income ratio, trust level, and how merged your financial lives are:

| Model | How It Works | Best For | Complexity |

| Fully Joint | All income goes to shared accounts. All expenses paid jointly. One budget. | Couples with similar incomes, strong trust, full financial merge | Low |

| Fully Separate | Each partner manages own income. Shared bills split by agreed formula. | Independent-minded couples, significant income disparity | Medium |

| Hybrid (Most Popular) | Shared account for joint expenses (rent, groceries, holidays) + individual accounts for personal spend. | Most modern couples — gives autonomy + shared accountability | Low-Medium |

The hybrid model works for most couples because it provides shared accountability for joint expenses while preserving each partner’s personal financial autonomy. You each have ‘yours, mine, and ours’ accounts.

Step 3: Set Up Your Shared Budget in EMOH Pay

EMOH Pay is built for household budgeting. Its member-tagging feature lets both partners see a unified household picture while still tracking who spent what. Here’s how to set it up:

- Both partners download EMOH Pay

- Connect all relevant bank accounts — joint accounts, individual accounts, joint credit cards

- Create household expense categories: Rent/Mortgage, Groceries, Utilities, Subscriptions, Dining, Transport

- Create individual spending categories per partner: ‘Partner 1 Personal’, ‘Partner 2 Personal’

- Tag transactions to the right person using EMOH Pay’s member tagging feature

- Set shared savings goals — holiday fund, home deposit, emergency fund — that both partners can see updating in real time

See how member tagging works: → EMOH Pay Features

Step 4: Agree on How to Split Joint Expenses

The fairest split depends on your income ratio. If both partners earn roughly the same, a 50/50 split is cleanest. If incomes differ significantly, a proportional split avoids resentment:

| Split Method | Formula | Best When |

| 50/50 Equal Split | Each pays half of all shared expenses | Incomes within 20% of each other |

| Proportional Split | Each pays their income % of shared expenses. If Partner A earns 60% of total household income, Partner A pays 60% of shared bills. | Significant income difference — feels equitable to both |

| Fixed Contribution | Each transfers a fixed amount to joint account monthly regardless of exact split | Simple households with predictable expenses |

| Income-Based Tithe | Each contributes a fixed % of their own salary (e.g. 30%) to the joint pot | Flexible — scales automatically with raises or income changes |

Step 5: Build Shared Financial Goals

Couples who share explicit, visible financial goals argue about money less. When both partners can see the holiday fund growing in EMOH Pay, impulsive spending feels less appealing because you’re both watching the same goal.

Set at minimum three shared goals in EMOH Pay:

- Short-term (0–12 months): Emergency fund (3 months of expenses), holiday fund, car maintenance fund

- Medium-term (1–5 years): House deposit, wedding fund, maternity/paternity leave buffer

- Long-term (5+ years): Retirement contributions, children’s education fund, financial independence target

How to set goals in EMOH Pay: → EMOH Pay Solutions

The ‘No-Surprises’ Rule: Spending Agreements

Most financial arguments start not with big purchases but with small, unexpected ones. The ‘no-surprises rule’ prevents this: agree on a spending threshold above which either partner checks in before purchasing.

Typical thresholds by relationship stage:

- Early relationship / living together: $50–$100

- Established couple with joint finances: $150–$300

- Long-term partners with high trust: $300–$500

The exact number matters less than having one. EMOH Pay’s real-time notifications mean both partners are alerted when large transactions hit any shared account — making surprises rare.

Dealing With Income Inequality

When one partner earns significantly more than the other, the proportional split method (above) handles the bills fairly. But income inequality can still create power dynamics around discretionary spending.

The most effective solution: both partners receive an equal monthly personal allowance from the household pot, regardless of who earns what. Each can spend their allowance on anything without justification. This preserves autonomy and eliminates the guilt or resentment that often follows income-unequal relationships.

Related: → Best Budgeting App for Families in 2026

Frequently Asked Questions

Q: Should couples have joint or separate bank accounts?

Both work — what matters is shared visibility, not a shared account. Many couples find the hybrid model most practical: a joint account for shared expenses (rent, groceries, utilities, holidays) and individual accounts for personal spending. EMOH Pay lets you connect and track all accounts in one dashboard regardless of how they’re structured.

Q: How do you budget when partners have very different incomes?

Use the proportional contribution method: each partner pays the same percentage of their income toward shared expenses. If Partner A earns £60,000 and Partner B earns £40,000, Partner A covers 60% of shared bills and Partner B covers 40%. This feels equitable to both parties.

Q: What is the best budgeting app for couples?

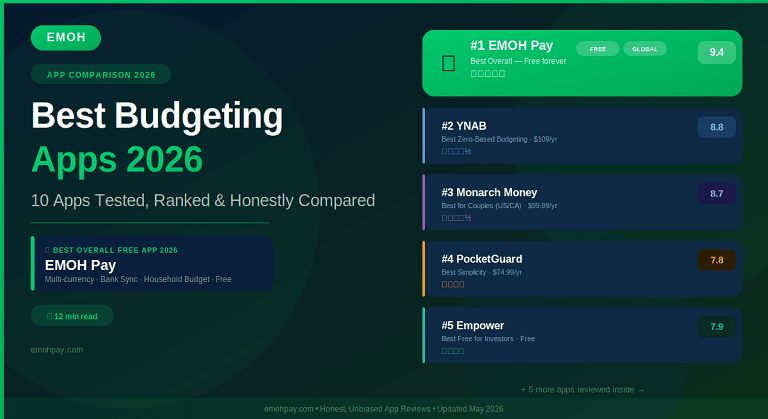

EMOH Pay is the best free budgeting app for couples in 2026. It supports household member tagging so each partner can see their individual spending contribution alongside the shared picture. Monarch Money is the best paid option for couples in the US and Canada.

Q: How do you talk to a partner about budgeting without it turning into a fight?

Frame it as a shared project (‘How do we build our financial future?’) rather than an audit (‘Where did you spend all the money?’). Use a monthly money date with neutral, shared data — EMOH Pay’s reports are excellent for this because both partners are looking at facts, not one partner’s interpretation of facts.

| Ready to Take Control of Your Finances?

Download EMOH Pay Free — Available on iOS & Android App Store: apps.apple.com/pk/app/emoh/id6743326641 Google Play: play.google.com/store/apps/details?id=com.buildmeapp.emoh |

More Guides for Household Finances

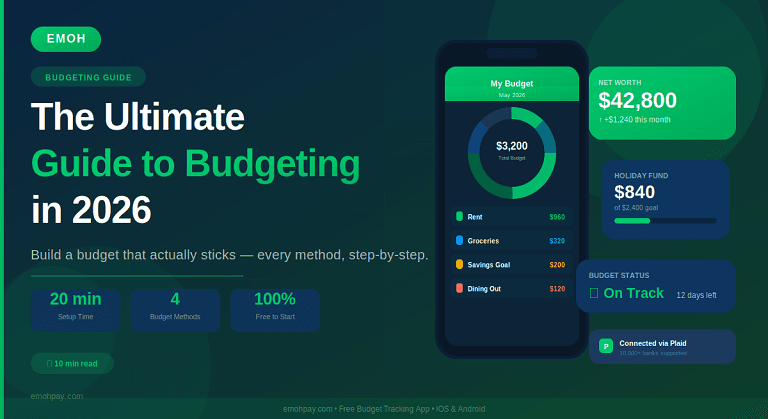

→ The Ultimate Guide to Budgeting in 2026

→ Best Budgeting App for Families in 2026

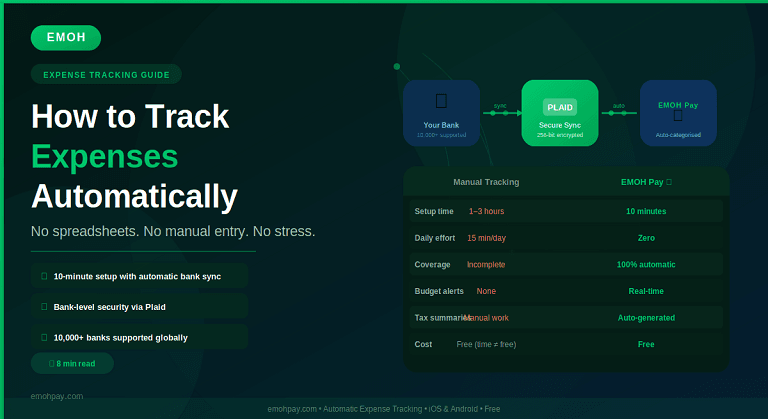

→ How to Track Expenses Automatically