Saving for our dream house felt overwhelming at first. Every time we looked at home prices, calculated a down payment, or thought about closing costs, the number felt bigger than our motivation.

And that is exactly why most people delay the process.

The problem is not income. The problem is unclear math and no system.

In this guide, you will learn how saving for our dream house becomes simple when you break it into clear numbers, realistic timelines, and a weekly system you can actually follow. No fluff. Just a practical roadmap.

Why Saving for Our Dream House Feels So Hard

Most families make three common mistakes:

- They only think about the down payment savings

- They do not calculate total house related costs

- They try to “save what is left” instead of planning first

Saving for our dream house is stressful because the goal is emotional. It is not just a purchase. It is security, pride, stability, and a future.

But emotions do not replace math.

Once you turn the dream into numbers, the stress drops dramatically.

Step 1: Calculate Your Real House Savings Target

Saving for our dream house includes more than a down payment.

Your complete target should include:

- Down payment savings

- Closing costs

- Moving expenses

- Initial repairs or furniture

- A safety cushion after purchase

If you only save for the down payment, you will feel behind the moment extra costs appear.

Simple Formula

Total House Fund Needed =

Down Payment + Closing Costs + Moving + Cushion

Now subtract what you already have saved.

That is your real target.

Step 2: Turn the Big Number Into a Monthly Goal

Saving for our dream house becomes manageable when you break it into months.

Monthly Savings Goal =

(Remaining Target) ÷ (Months Until Purchase)

Example:

- Total target: 60,000

- Already saved: 10,000

- Remaining: 50,000

- Timeline: 25 months

Monthly goal = 2,000

Now it is no longer “a huge dream.”

It is a clear monthly commitment.

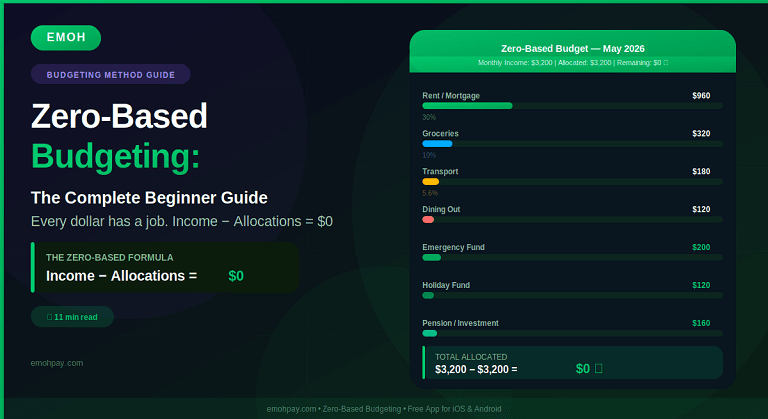

Step 3: Build a Monthly Budget Plan That Supports the Goal

If you are serious about saving for our dream house, your budget must reflect it.

Structure your monthly budget like this:

1. Fixed Expenses

- Rent

- Insurance

- Loan payments

2. Variable Essentials

- Groceries

- Utilities

- Transportation

3. Flexible Spending

- Dining out

- Shopping

- Entertainment

4. House Savings Contribution (Non Negotiable)

Your house savings plan should come before lifestyle spending, not after.

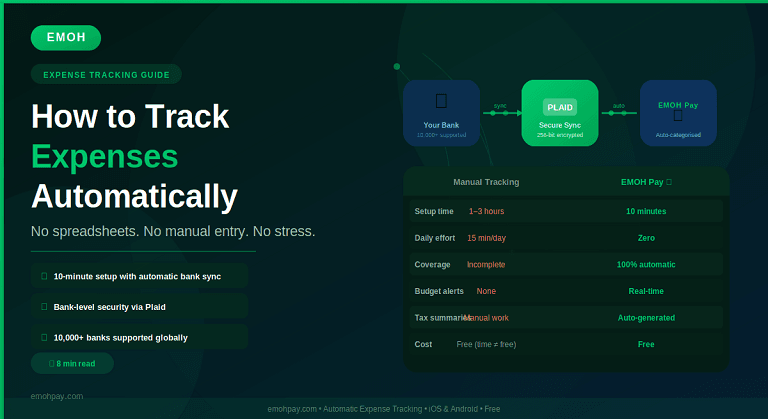

Step 4: Track Spending Without Overcomplicating It

You cannot improve what you do not measure.

Saving for our dream house requires visibility.

Focus on these common “budget leaks”:

- Food delivery creep

- Subscription renewals

- Impulse shopping

- Convenience spending

- Unplanned events

Even small adjustments can free up hundreds each month.

This is where structured category budgeting helps. Platforms like EMOH Pay are designed to simplify expense tracking, savings goals, and monthly budget planning in one place so households can clearly see where money is going without juggling spreadsheets.

Clarity reduces stress.

Step 5: Automate Your Down Payment Savings

Automation removes emotion from the process.

Set up automatic transfers right after payday.

Treat your house fund like a bill you owe your future.

When saving for our dream house becomes automatic, consistency improves instantly.

Step 6: Increase Savings Without Feeling Miserable

You do not need extreme sacrifices. You need focused adjustments.

High impact strategies:

- Save a percentage of bonuses and tax refunds

- Temporarily reduce one lifestyle category

- Pause non essential subscriptions

- Direct side income straight to the house fund

- Negotiate recurring bills

Short term discipline creates long term stability.

Step 7: Protect Your Emergency Fund

One major mistake people make while saving for our dream house is draining their emergency savings.

Never use your entire financial cushion for a down payment.

A home brings new responsibilities:

- Repairs

- Maintenance

- Insurance adjustments

Security first. Always.

Saving for Our Dream House as a Couple

Money stress often comes from misalignment.

If you are saving for our dream house with a partner:

- Agree on one clear target

- Set a shared timeline

- Review progress weekly

- Assign budget categories to each person

Shared goals reduce conflict.

When both partners can see progress clearly through a budgeting system, motivation increases and arguments decrease.

Where Should You Keep Your House Savings?

If your timeline is short, prioritize safety and accessibility.

Options many people consider:

- High yield savings accounts

- Dedicated house savings accounts

- Separate digital savings buckets

Avoid high volatility investments if you plan to buy soon.

Protect the dream from unnecessary risk.

Common Mistakes That Delay Homeownership

- Waiting to “start later”

- Not tracking expenses

- Underestimating closing costs

- Ignoring small daily spending

- Changing the goal every few months

Saving for our dream house requires consistency, not perfection.

What Changes Everything

The biggest mindset shift is this:

Stop saying “We cannot afford it.”

Start asking “What system would make this possible?”

When you:

- Know your exact number

- Follow a structured monthly budget

- Automate savings

- Track spending weekly

Saving for our dream house becomes predictable instead of stressful.

Frequently Asked Questions

How much should we save for a dream house?

It depends on the home price, loan type, and location. At minimum, plan for a down payment, closing costs, moving expenses, and a financial cushion.

Is 20 percent down required?

No. Many loan programs allow lower down payments. However, higher down payments can reduce monthly costs and eliminate mortgage insurance.

How long does saving for our dream house take?

It depends on income, home prices, and savings rate. A clear monthly savings plan shortens the timeline significantly.

What is the best way to save for a down payment?

Automate transfers, reduce budget leaks, increase income if possible, and track spending consistently.

Should we invest our house savings?

If you plan to buy within a few years, prioritize stability over growth. Volatility can delay your purchase.

How do couples avoid money arguments while saving?

Set shared goals, track expenses transparently, review progress weekly, and use a budgeting system that both can access.

What if our monthly goal feels too high?

Adjust one of three levers:

- Extend timeline

- Increase income

- Lower purchase price range

Do we need a budgeting app?

You need a clear system. Whether it is a spreadsheet or a structured budgeting platform, clarity and consistency matter most.

Final Thoughts

Saving for our dream house sounded stressful at first.

But once we calculated the real target, built a realistic monthly budget plan, automated savings, and tracked expenses clearly, everything changed.

The dream did not shrink.

The system improved.

If you want a structured way to track spending, manage savings goals, and stay aligned as a household, you can explore tools designed for this purpose like EMOH Pay at: https://emohpay.com/.

Also download the EMOH Pay app from Google Play and App Store.

Clarity creates confidence.

Confidence builds homes.