Creating a budget is one of the most impactful steps you can take to gain control over your finances. Whether you’re aiming to save for a big purchase, eliminate debt, or simply manage your money better, budgeting is the foundation of financial success. This guide will walk you through how to make a budget step by step, so you can feel empowered and in control of your financial future.

Why Budgeting Matters

At its core, a budget is your financial roadmap. It shows where your money comes from, how it’s spent, and where you can make adjustments. With a solid budget, you can:

- Reduce financial stress

- Save for future needs

- Avoid unnecessary debt

- Achieve long-term financial security

Whether you’re tackling student debt in Toronto or saving for a family trip, budgeting is the key to turning your financial dreams into reality. For even more insights on why budgeting matters, check out Canada.ca’s introductory guide to budgeting.

Step 1: Assess Your Financial Situation

Before building any plan, it’s essential to understand where you stand. Here’s how you can assess your financial health:

- Calculate your net income

This is the money you receive after taxes, benefits, and deductions are taken out. It’s the baseline for your budget.

- List all debts or liabilities

Include credit card balances, student loans, or car payments. If you’re feeling overwhelmed or stressed about financial decisions, consider exploring “therapy near me in Toronto” to support your mental well-being while you manage your money.

- Determine your assets

Note your savings, investments, and valuable possessions to better understand your financial worth.

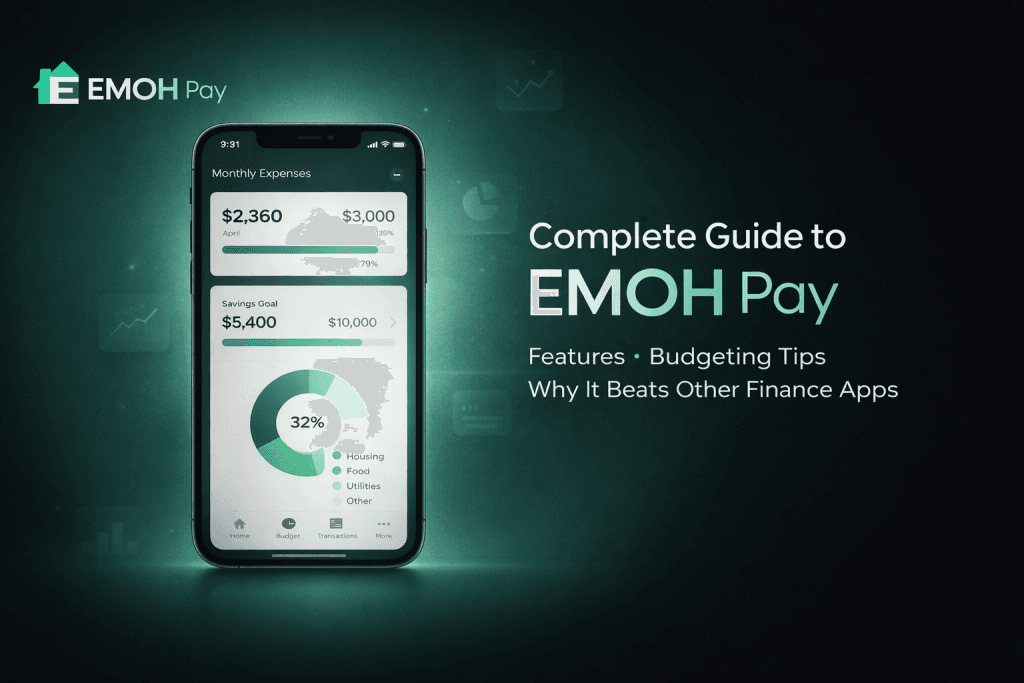

You can also use innovative budgeting apps like EMOH PAY to easily track your financial snapshot in one place. By knowing your starting point, you can build a realistic budget tailored to your needs.

Step 2: Set Clear Financial Goals

What do you want your budget to achieve? Setting specific, measurable goals ensures your financial efforts are focused. Examples include:

- Saving $500 per month for an emergency fund

- Paying off $10,000 in credit card debt within a year

- Allocating $200 per month for a family getaway

Tip: Write down your goals and prioritize them. For instance, tackle high-interest debt before setting aside money for luxuries. For goal-setting resources.

Apps like EMOH PAY allow you to set and monitor multiple financial milestones within one dashboard, keeping you accountable as you work toward your objectives.

Step 3: Track Your Income and Expenses

Tracking is the backbone of budgeting. Here’s how to do it effectively:

- Record your income sources

Include your main salary, side hustles, rental income, or any other earnings.

- Track your expenses over a month

Use a budgeting app like EMOH PAY or a simple spreadsheet to categorize each expense. Include everything from rent to morning coffee runs. For additional tracking techniques.

Many people are surprised to learn how much they spend on “non-essentials.” This awareness plays a crucial role in reshaping spending habits.

Step 4: Categorize Your Spending

Divide your expenses into fixed and variable categories to clarify your financial picture:

- Fixed expenses

Mortgage/rent, debt payments, insurance, and utility bills.

- Variable expenses

Eating out, entertainment, retail shopping, and fuel.

Suggestion: The 50/30/20 rule is a popular budgeting guideline. Allocate 50% of your income to needs, 30% to wants, and 20% to savings or debt repayment.

Using EMOH PAY’s customizable categories makes this process even easier, offering charts and summaries that visualize your spending breakdown at a glance.

Step 5: Choose a Budgeting Method

There’s no one-size-fits-all approach when it comes to budgeting. Consider these common methods and find one that works for your lifestyle:

- Zero-based budgeting

Every dollar is assigned a job. At the end of the month, your income minus expenses should equal zero.

- Envelope system

Use physical or digital “envelopes” for each spending category. When the envelope is empty, no more spending!

- Pay yourself first

Allocate savings or investment amounts before spending.

Experiment with different systems to learn which aligns with your personality and goals. For more options, see NerdWallet’s guide to budgeting methods.

You can experiment with these different approaches within apps like EMOH PAY, which adapts to your chosen structure and provides instant feedback.

Step 6: Adjust and Reassess Your Budget Regularly

Life changes, and so should your budget. Update your budget to reflect any shifts in:

- Income (e.g., promotions, job changes)

- Expenses (e.g., new subscriptions, moving costs)

- Goals (e.g., upcoming vacations or milestones)

Set a monthly calendar reminder to review your spending and ensure you’re staying on track. EMOH PAY offers reminders and alerts to help you stick to your goals efficiently.

FAQs:

1. What is the best budgeting app in Canada?

Popular apps like Mint, You Need a Budget (YNAB), PocketSmith, and EMOH PAY are excellent choices for Canadians. They help you track income and expenses effortlessly. For independent reviews.

2. How often should I revisit my budget?

At a minimum, review your budget monthly. For significant life changes, review it immediately. Tools like EMOH PAY provide automatic prompts for regular budget check-ins.

3. Can budgeting reduce financial stress?

Absolutely. A well-structured budget gives you control over your money, reducing uncertainty about bills or expenses. For deeper emotional challenges related to finances, using a smart budgeting app like EMOHpay can help you feel more in control and less overwhelmed.

4. Is it hard to stick to a budget?

It can be challenging, especially at first. Start small, set realistic goals, and track progress to build confidence and consistency. Supportive platforms like EMOH PAY break down your budgeting journey into manageable steps.

Next Steps and Resources

Now that you know how to make a budget, it’s time to take action! Use these strategies to craft a financial plan today and start reaping the benefits.