Managing money together can be one of the biggest challenges a couple faces. Conversations about finances can feel stressful, but creating a shared financial plan is a powerful way to build a strong foundation for your future. Effective budgeting for couples isn’t just about tracking dollars and cents; it’s about communication, shared goals, and teamwork.

This guide will walk you through the essential steps to create a budget that works for both of you. We’ll explore different methods for managing your money, setting achievable goals, and using tools to simplify the process. By the end, you’ll have a clear roadmap for achieving financial harmony in your relationship.

Why is Budgeting for Couples So Important?

Money is a leading cause of stress in relationships. When you and your partner aren’t on the same page financially, it can lead to arguments, resentment, and a lack of trust. Creating a budget together helps prevent these issues by fostering open communication and transparency.

A shared budget aligns your financial habits and helps you work towards common objectives, whether that’s buying a home, saving for a vacation, or paying off debt. It transforms money from a source of conflict into a tool for building the life you both want. Proper money management in relationships is a key pillar of a successful partnership.

Getting Started: The Money Talk

Before you can build a budget, you need to have an open and honest conversation about your finances. This isn’t a one-time chat but an ongoing dialogue. Find a calm, relaxed time to sit down together, free from distractions.

Key Topics to Discuss:

- Financial History: Share your personal history with money. How did your family handle finances? What lessons, good or bad, did you learn?

- Income and Debt: Be transparent about your individual incomes, savings, and any outstanding debts (student loans, credit card balances, etc.).

- Spending Habits: Talk about your spending triggers and priorities. Are you a saver or a spender? What do you value spending money on?

- Financial Goals: Discuss your short-term and long-term dreams. Do you want to travel, invest, buy a house, or retire early?

This conversation builds a foundation of trust and understanding. Remember to be empathetic and non-judgmental. The goal is to get on the same team, not to criticize each other’s past financial decisions.

Choosing Your Budgeting Method

There is no single “best” way to manage finances as a couple. The right approach depends on your comfort levels, income levels, and personal preferences. Let’s explore the most common methods.

1. Joint Accounts: The “All-In” Approach

Many couples choose to merge their finances completely by opening a joint checking and savings account. All income goes into these accounts, and all bills are paid from them.

- Pros: This method promotes ultimate transparency and teamwork. It simplifies bill payments and makes tracking shared spending easy.

- Cons: It can feel like a loss of financial independence for some. If spending habits differ greatly, it can cause friction.

2. Separate Accounts: The “Yours and Mine” Approach

In this setup, you both maintain your individual bank accounts. You then decide how to split shared bills. This method is common for couples who want to maintain their financial autonomy.

- Pros: Each partner maintains control over their personal spending. It works well if you have significant differences in income or spending styles.

- Cons: It can be complicated to track and pay shared expenses in Canada. It requires constant coordination to ensure bills are paid on time.

3. The Hybrid Approach: “Yours, Mine, and Ours”

This method offers a popular middle ground. You each keep your separate accounts for personal spending but also open a joint account for shared household expenses like rent, utilities, and groceries.

- Pros: This approach balances independence with teamwork. It simplifies bill payments while allowing each partner personal spending freedom.

- Cons: It requires deciding what constitutes a “shared” expense versus a “personal” one, which can sometimes be a gray area.

FAQ Answer: Should couples have joint or separate budgets?

This depends on your comfort level; many couples succeed with joint accounts for shared bills and separate accounts for personal spending (a hybrid approach).

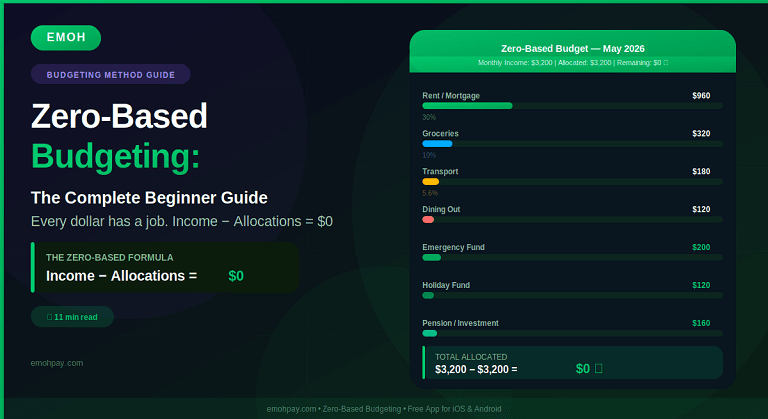

How to Build Your Couple’s Budget in 5 Steps

Once you’ve chosen a method, it’s time to build your budget. This is where effective couple finance planning Canada comes into play.

Step 1: Calculate Your Total Household Income

Add your individual net incomes (after taxes) together to get your total monthly household income. This is the starting point for your budget.

Step 2: Track Your Expenses

For one month, track every single expense. This includes fixed costs like rent/mortgage and utilities, as well as variable costs like groceries, entertainment, and personal shopping. This step is crucial for understanding where your money is actually going.

Step 3: Categorize Your Spending

Group your expenses into categories (e.g., Housing, Transportation, Food, Debt Repayment, Personal Care, Entertainment). This helps you see which areas are consuming the largest portions of your income.

Step 4: Set Spending Limits and Goals

Review your spending categories together. Are there areas where you can cut back to free up more money for your goals? Assign a realistic spending limit to each category. This is the core of budgeting for couples: making intentional decisions about your money together.

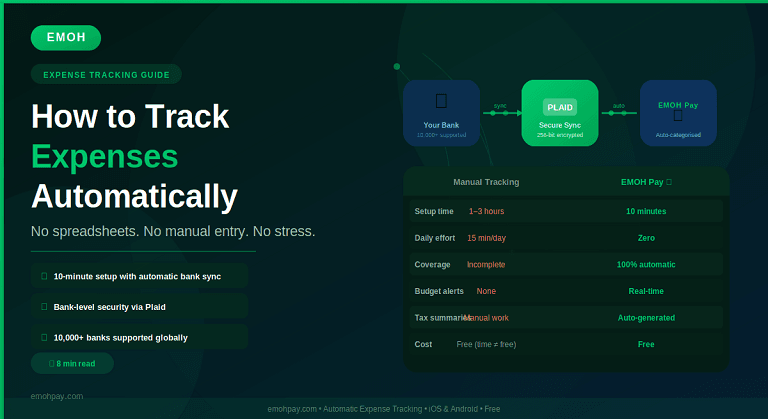

Step 5: Use a Budgeting App

Manually tracking expenses can be tedious. A budgeting app can automate the process, making it easier to stick to your plan. Tools specifically designed for shared expenses can be a game-changer. For example, using an app like Emoh Pay can help you seamlessly track and split costs, reducing the mental load of managing shared finances.

FAQ Answer: What’s the best app for sharing expenses?

The best app simplifies tracking and splitting costs; tools like Emoh Pay are designed specifically to help partners and roommates manage shared expenses easily.

Setting Financial Goals as a Couple

A budget without goals is just a spending plan. Your goals are the “why” behind your budget. They provide motivation to stick to your plan, even when it’s tempting to overspend.

Divide your goals into three categories:

- Short-Term (1-2 years): Building an emergency fund (3-6 months of living expenses), paying off a high-interest credit card, or saving for a vacation.

- Mid-Term (3-5 years): Saving for a down payment on a home, upgrading your car, or planning a wedding.

- Long-Term (5+ years): Saving for retirement, paying off your mortgage early, or funding your children’s education.

FAQ Answer: How do we set financial goals as a couple?

Start by openly discussing your individual and shared dreams, then categorize them into short-term, mid-term, and long-term objectives with clear, measurable targets.

Fairly Managing Money Together

Fairness in finances doesn’t always mean a 50/50 split, especially if there’s a significant income disparity. A more equitable approach is to contribute proportionally.

For instance, if one partner earns $60,000 and the other earns $40,000, your total household income is $100,000. Partner A earns 60% of the income, and Partner B earns 40%. You could then agree to split shared expenses 60/40. This ensures that both partners contribute a fair percentage of their income and have a similar amount of discretionary money left over.

FAQ Answer: How can couples manage money together fairly?

Fair management often involves contributing to shared expenses proportionally to your income, rather than splitting everything 50/50, to ensure equity.

Review and Adjust Regularly

Your budget is not a static document. It’s a living plan that should evolve with your life. Schedule a monthly “budget date” to review your spending, track your progress toward goals, and make any necessary adjustments. Life changes—a new job, a raise, or an unexpected expense—will require you to revisit and tweak your budget.

These regular check-ins are also a great opportunity to celebrate your financial wins. Did you stick to your budget? Did you hit a savings goal? Acknowledging your progress reinforces your teamwork and keeps you motivated.

Conclusion:

Successful budgeting for couples is less about spreadsheets and more about communication, shared values, and mutual respect. By talking openly about money, choosing a system that works for you, setting meaningful goals, and regularly reviewing your progress, you can turn financial management into a collaborative and empowering part of your relationship.

With the right mindset and tools, you can build a strong financial future together. Start the conversation today and take the first step toward mastering your finances as a team.