Taking control of your money can feel like a monumental task. You work hard for your income, but at the end of the month, do you ever wonder where it all went? If you’re looking for a proactive way to manage your finances and give every dollar a job, the answer might be found in a powerful method: zero-based budgeting. This approach helps you gain clarity and control over your spending, ensuring your money aligns with your goals.

This guide will walk you through the fundamentals of zero based budgeting personal finance. We will explore how it works, why it’s so effective for beginners, and how modern tools can simplify the entire process. By the end, you will have a clear roadmap to start your own journey toward financial wellness.

Understanding the Zero-Based Budgeting Method

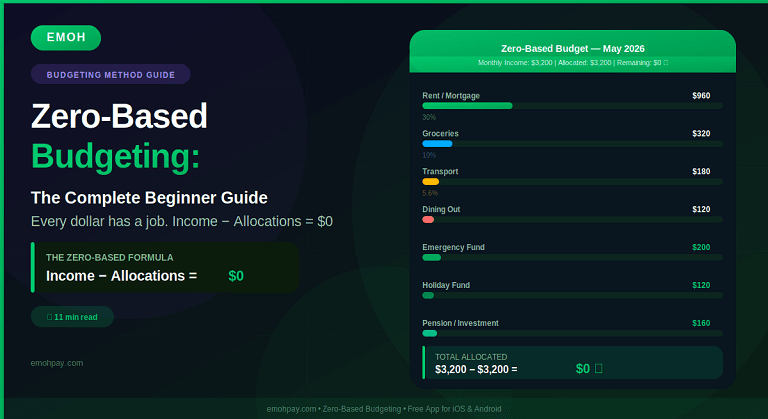

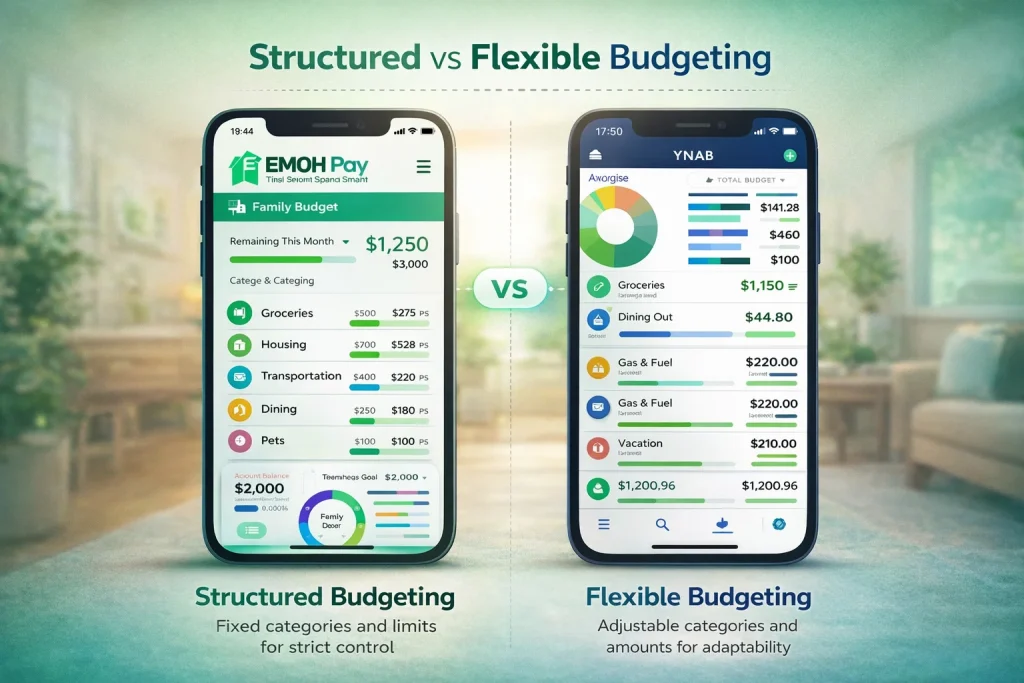

At its core, zero-based budgeting is a simple concept. It’s a system where your income minus your expenses equals zero. This doesn’t mean you spend everything you earn until your bank account is empty. Instead, it means you purposefully budget every dollar allocate expense. Every single dollar that comes in is assigned a specific role, whether that’s for bills, groceries, savings, debt repayment, or investments.

Think of your monthly income as a team of employees. With a zero-based budget, you become the manager, giving each “employee” (each dollar) a specific task to complete. No dollar is left idle or unaccounted for. This method forces you to be intentional with your spending and saving habits. Unlike traditional budgeting where you might just track past spending, this system requires you to plan for the future, one month at a time.

How Does It Differ From Traditional Budgeting?

Traditional budgeting often involves looking at last month’s spending and adjusting it slightly for the current month. For example, if you spent $400 on groceries last month, you might budget the same amount for this month. The weakness here is that it can lead to mindless spending and perpetuate habits that don’t serve your financial goals.

Zero-based budgeting, on the other hand, starts from scratch each month. You justify every expense, forcing you to ask, “Is this purchase necessary? Does it align with my priorities?” This level of scrutiny helps you identify and eliminate wasteful spending, freeing up more money for things that truly matter, like building an emergency fund or saving for a down payment on a house.

Getting Started with Zero-Based Budgeting: A Step-by-Step Guide

Embarking on a zero based budgeting personal finance journey is easier than you might think. It requires some initial effort, but the long-term benefits of financial clarity and control are well worth it.

Step 1: Calculate Your Total Monthly Income

First, you need to know exactly how much money you have to work with. Add up all your sources of income for the month. This includes your regular paycheck after taxes, any side hustle income, and any other cash you expect to receive. If your income varies, it’s best to use a conservative estimate or the lowest amount you’ve earned in recent months. This ensures you don’t budget money you don’t have.

Step 2: List All Your Monthly Expenses

Next, create a comprehensive list of all your anticipated expenses for the month. It’s helpful to break these down into categories:

- Fixed Expenses: These are consistent costs that rarely change, like rent or mortgage payments, insurance premiums, and loan payments.

- Variable Expenses: These are costs that fluctuate, such as groceries, utilities, transportation, and entertainment. Review your bank and credit card statements from the past few months to get a realistic idea of what you typically spend in these areas.

- Irregular Expenses: Don’t forget about expenses that don’t occur every month, like car maintenance, annual subscriptions, or holiday gifts. It’s wise to set aside a small amount each month into a “sinking fund” for these.

- Savings and Investments: Treat your savings goals as non-negotiable expenses. This includes contributions to your emergency fund, retirement accounts, or other investment goals.

Step 3: Allocate Your Income Until It Reaches Zero

Now for the main event. Start assigning your income to the expense categories you listed. Begin with your essential needs—housing, food, utilities, and transportation. Then, allocate funds to your financial goals, like debt repayment and savings. Finally, distribute the remaining money to your wants, such as dining out, hobbies, and entertainment.

The goal is to make your income minus your allocated expenses equal zero. If you have money left over, don’t just leave it sitting there! Assign it a job. You could put extra toward a debt, boost your savings, or invest it. If you find your expenses exceed your income, you need to make adjustments. Look for areas in your variable spending where you can cut back.

Step 4: Track Your Spending and Adjust

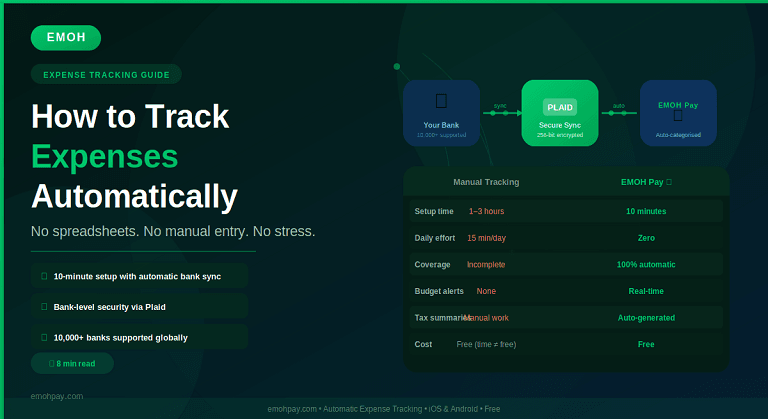

A budget is not a “set it and forget it” document. Throughout the month, you must track your spending diligently to ensure you’re staying on course. This is where many people stumble, as manual tracking can be tedious. This is also where beginner budgeting app strategies become incredibly valuable.

Using an app simplifies tracking and gives you a real-time view of your financial situation. If you overspend in one category, you can see it immediately and adjust by moving funds from another non-essential category to cover the difference. At the end of the month, review what worked and what didn’t. Each month is a new opportunity to refine your budget and get better at managing your money.

Leveraging Technology for Success

Manually managing a zero-based budget with spreadsheets can be time-consuming. Fortunately, technology has made it much simpler. Budgeting apps automate much of the process, from tracking expenses to visualizing your progress.

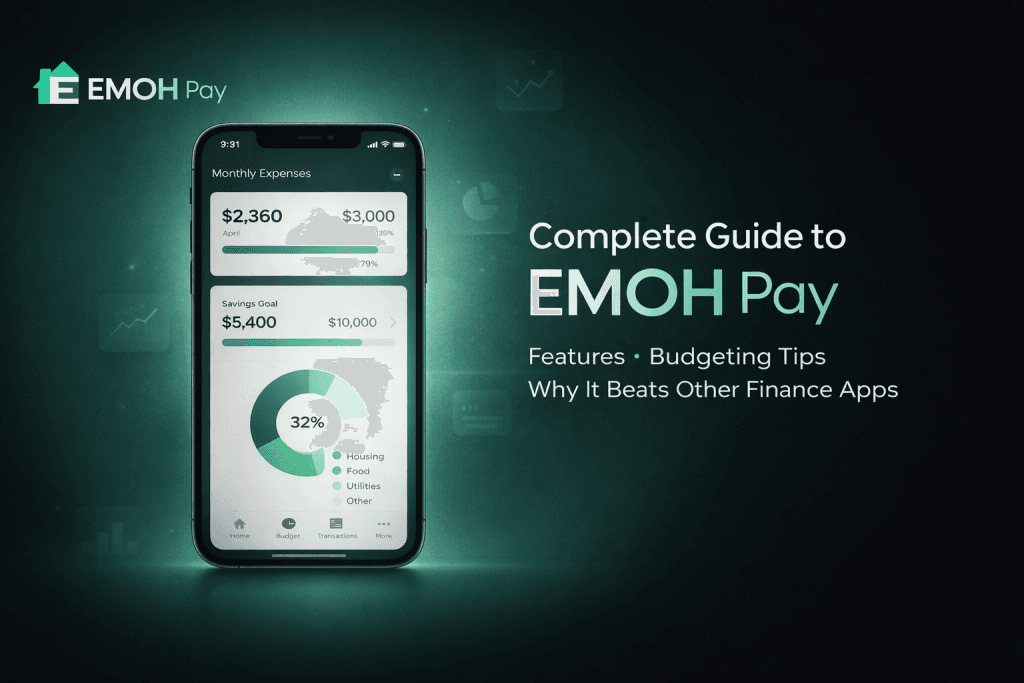

An effective app can connect to your bank accounts, automatically categorize transactions, and show you how much you have left to spend in each category. This makes the entire process more engaging and less of a chore. For those new to this method, finding a tool with a dedicated Emoh Pay zero-based feature can be a game-changer. By using a platform designed for this specific strategy, you can streamline your workflow and focus on making smart financial decisions.

The Emoh Pay app, for example, is designed to help users implement budgeting strategies with ease. It provides the tools you need to create a plan, track your progress, and ultimately achieve your financial objectives. By connecting your accounts, you get a clear, up-to-date picture of your finances, allowing you to manage your zero-based budget effectively.

The Long-Term Benefits of a Zero-Based Budget

Adopting this detailed approach to zero based budgeting personal finance offers more than just a balanced checkbook. It transforms your relationship with money. You’ll develop a heightened awareness of your spending habits, enabling you to plug financial leaks you never knew you had. This method empowers you to be the boss of your money, directing it toward what you value most.

Over time, you will build strong financial discipline, reduce money-related stress, and make significant progress toward your most important life goals. Whether you want to become debt-free, buy a home, or retire early, a zero-based budget provides the framework to make it happen. It’s a proactive, forward-looking strategy that puts you firmly in the driver’s seat of your financial future.

Frequently Asked Questions

What is zero-based budgeting and how does it work?

It’s a budgeting method where you plan for every dollar of your income, ensuring that your income minus all your expenses (including savings and debt payments) equals zero.

How can budgeting apps implement zero-based budgeting?

Budgeting apps can link to your bank accounts to track income and expenses in real-time, allowing you to create categories and allocate every dollar to a specific purpose.